It is often said that value can be had for those willing to get their hands dirty. This is certainly the case for industries such as waste or scrap removal, but it also very much applies to niche recovery opportunities in the mining services sector. Enter: Goldplat (GDP), a micro-cap gold recovery services business with related operations in South Africa, Ghana, and Burkino Faso.

Goldplat’s market is attractive primarily because of its high barriers to entry which derives from: a) the required scale of operations for profitability, and b) the technological know-how and specialist expertise for gold extraction from mine residue and waste. This in itself discourages miners from processing their own waste, leaving an indefinite services opportunity for those with the capability. Goldplat is leading the way in this respect.

Goldplat’s Operations

The niche services company has numerous contracts with various mining entities whereby it purchases mine residues and waste at an agreed price, often linked to the prevailing gold spot price. Thus, in the long run, Goldplat is not adversely affected by a falling gold price as its margin simply moves in line with the market price of gold. Saying that, we should note that the spot price for gold naturally moves far quicker than the company’s contract renewal process. Therefore, a falling gold price will initially impact those contracts agreed at the historically higher gold price, meaning that those contracts’ margins will be squeezed until the contracts are renegotiated to account for the lower gold price environment.

Conversely though, a rising gold price will materially temporarily improve margins, and Goldplat has a unique quality in that it can choose when to sell its recovered gold on the open market. The company can opt to store its gold in inventory until a more attractive gold market presents itself. The limiting factor to this strategy would be liquidity, however.

Recent Developments

- GDP announces that the 6 month period to 31 December 2013 had been “difficult” due to a “lower gold price environment” as well as a number of “temporary factors that have affected parts of the Company’s operations”

- A number of welcome initiatives were introduced to improve efficiencies and therefore profitability, including:

- the cancellation of low grade contracts which are unprofitable at a low gold spot price

- the revision of by-product procurement contracts to reflect a lower gold price

- Further business initiatives have been implemented to drive earnings:

- Cyanide had previously been purchased via intermediaries in solid form. This has been replaced with local suppliers who can offer cyanide in liquid form, making significant cost savings to Goldplat from October 2013

- The intention to actively stockpile by-product reserves will provide production optionality and further cost savings, as Goldplat will be able to purchase in bulk and enjoy economies of scale benefits

- The company was awarded the Responsible Gold producer certificate. Goldplat is the first secondary gold producer to obtain this status in South Africa. It is expected that this commendable title will have a “significant and positive impact on future contracts, profits and cash flows”

All three of GDP’s profit centres in its recovery operation in Ghana (Gold Recovery Ghana) have experienced various operational challenges over the last year or so but the worst appears to have been resolved, promising for a stronger and more profitable next financial year

Finally, it is worth including here the upbeat and optimistic view offered by management:

“The company is confident that it can expand its business benefiting from the tax free status substantially into the rest of Africa and even further afield, and will work to achieve this during the remainder of 2014”

Shareholder Plight

The story so far has been one of a typical turnaround: a strong business model, protective barriers to entry, and a number of challenges, temporary in nature, which offer an attractive window of opportunity for new investors. However, not all is so rosy, if private investor bullet-in boards are anything to go by. The general market perception appears to be increasingly sceptical regarding the management of the company, and whether they are acting in the best interests of shareholders.

It is quite worrisome that the company has had three CEOs since September 2012, although it is pleasing to see the recent appointment and promotion of Hansie van Vreden to Chief Operating Officer, a position which had not existed prior to. A role dedicated to operations is vital for a business model such as this, and puts the company in better stead going forward.

The current CEO is Ian Visagie, an accountant by profession, who has been with the company since 2000 when he took over management control of Goldplat Recovery with Demetri Manolis. Mr Manolis was CEO until September 2012, when he believed it was “time to step down as the Company reaches the next stage of its genesis”.

The recent turbulence and uncertainty indirection borne from the changing management structure should be at an end, but the market will take time to accept this. This diminishing perception of uncertainty may perhaps be offering a good discount to enter the stock.

Financials

Goldplat’s interims are due out tomorrow and this should shed some light on the explicit effect the challenges of the first half of the year have had on the Company’s financials. Guidance so far has been that “operating profit for FY 2014 [is] to be materially below operating profit for FY 2013”. Operating profit (defined as gross profit before the deduction of expenses) for 2013 came in at £4.57m.

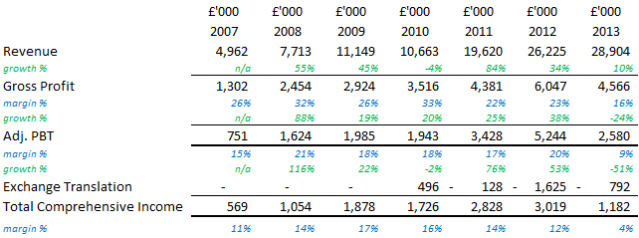

Profit after tax but before exceptional items for FY 2013 was £1.97m, 57% down on FY 2012’s £4.64m. Although revenues increased 10% over the same period from £26.23m to £28.90m, gross margins declined from 23% to 16%. This margin squeeze was the primary driver behind the declining profit and largely due to a falling gold price. See below for a summary of the company’s income performance:

It becomes clear that 2013 and 2014 together will be below-trend but, given that management have proactively sought improvements across operations and growth is still occurring, it is reasonable to expect a return to this impressive and dependable income schedule.

Valuation

Goldplat becomes a compelling investment proposition when we assess its value from a balance sheet perspective. Doing this, we find that the Company currently trades at a slight discount to its net-net working capital (N-NWC) position. The market cap at 5p stands at £8.4m, while the N-NWC position is an attractive £8.9m. The net-net working capital position is calculated by taking all the company’s liquid assets and taking out of this the Company’s entire liabilities (usually just the current assets are included, but a few non-current assets can also be included. Here, we chose to include the £1.96m for the ‘Proceeds from sale of shares in subsidiary’. Note that if we don’t include this then N-NWC < market cap).

This is a conservative and quick liquidation valuation method. It entirely ignores the Company’s property, plant and equipment, arguably the most valuable part to the Company’s business structure. Including all tangible assets, PPE therefore considered, we come to a net tangible asset value (NTAV) to market cap ratio of 0.54. Effectively, every £1 of investment in the company’s stock gives you £2 of hard assets. This is an attractive offering indeed.

Further, the Company’s intangibles are arguably of considerable value as they contain all the company’s mineral resource rights. The most recent (12 December 2012) JORC compliant estimation for Goldplat’s portfolio reported a resource of 931,071 oz AU. Since the strategic review these assets are considered non-core now, and there is the expectation that value will be realised by their eventual sale. This would certainly indicate the idea of a special dividend in the not-too-distant future.

Here is a quick preliminary valuation of the resource: Let’s assume a gold price of $1,200/oz, and an all-in sustaining cost of $1,000/oz. A conservative initial structure on both counts. With this, there is $200/oz net to Goldplat, if it were to mine these resources. Ignoring the time value of money and the significant risks attached to their extraction, this would value the reserve (if we assume that 25% of the resource is bumped up to the higher confidence level of measured and indicated) of around £28m. But, gold in the ground is always sold at a severe discount to its net realisable value, so lets reduce this by a further 75%, which gives us a price tag of £7m.

Although we made some heroic assumptions to come to this rudimentary estimation, remember that it did involve a conservative approach. Considering that this £7m is only a small discount to the entire market cap of the company, these assets are valued by the market at zero. And yet, they do have significant value.

NAV to market cap ratio comes in at 0.35, very much reflecting the value existent here.

Finally, Goldplat was required, in order to become BEE compliant (Black Economic Empowerment, a South African Government initiative) in South Africa, to sell a stake in their SA operation. This gave a read-across valuation of the entire subsidiary of £16m, about twice the current market cap of £8.4m. They certainly received a competitive price for the sale, but regardless, the SA subsidiary is one of three recovery operations Goldplat operates. Note that the SA operation is definitely the largest of the three, but also the one with the least growth opportunities. It is seen as a stable base of the company.

Conclusion

Together, these valuations certainly scream to the savvy investor of a very good deal indeed. Further, management think the same, to the extent that they brought online a share repurchase programme in an effort to drive the market cap value further towards intrinsic value.

It is very rare indeed to see a company trade at such a severe discount to NAV and remain profitable. Of course, tomorrow’s interims may throw this statement into invalidity, but from a long term perspective Goldplat offers probably one of the most attractive investments on AIM. We recommend a BUY for Goldplat Plc.

Shares in the pioneering gemstone miner dropped 5% upon open on Thursday after the Group released their final results for the year ending 30 June 2013. Operationally, the miner has excelled, driving down costs on all fronts and significantly building up inventories. Financially, however, the Group struggled to monetize its high value products due to the disruptions in their auction programme. It caused one fewer auctions to be held and thus lead to a 42% fall in revenues.

Shares in the pioneering gemstone miner dropped 5% upon open on Thursday after the Group released their final results for the year ending 30 June 2013. Operationally, the miner has excelled, driving down costs on all fronts and significantly building up inventories. Financially, however, the Group struggled to monetize its high value products due to the disruptions in their auction programme. It caused one fewer auctions to be held and thus lead to a 42% fall in revenues.